Analyzing a Sample Auto Loan Agreement

What is an Auto Loan Agreement?

An auto loan agreement is a legally binding contract between a borrower and a lender, outlining the terms and conditions of the loan for purchasing a vehicle. It serves as a road map for how the loan will be repaid, including the amount of the monthly payment and when it must be paid. Essentially, it defines the responsibilities of both the borrower and the lender in the car financing process. The borrower, often a car buyer, agrees to repay the loan according to the terms of the agreement . In return, the lender will extend credit under certain conditions.

Being familiar with an auto loan agreement can arm you with information that can help you avoid common financial pitfalls associated with car loans. Its purpose is to set clear expectations and establish a process in the event of default. Specifically, it addresses four main areas: the amount you owe, the time you have to pay, the interest, and whether collateral is required.

Essential Elements of an Auto Loan Agreement

A sample auto loan agreement will usually contain the following key components, whether a standard loan agreement or a retail installment contract.

Loan Amount

The first component is typically the amount of money to be loaned by the lender to the borrower. These amounts can vary widely, depending on the value of the vehicle, of course. Some contracts will also specify the amount of the down payment by the borrower, sometimes referred to as the deposit.

Interest Rate

Next to the loan amount, the most important component of a typical auto loan or leasing agreement is the interest rate. Interest rates on loans fluctuate from day to day and can change based on a number of factors, such as prime lending rates or dealer incentives. Some lenders may even offer fixed interest rate contracts, meaning that the conditions set at the time of the loan or lease will remain constant for the term of the agreement. Other contracts may specify a floating rate of interest, where repayments will adjust along with prevailing rates, either up or down.

Repayment Terms

In their most basic form, auto loan repayments require monthly installments over a period of months to years. Some leasing agreements, however, such as a rent-to-own stipulation, require weekly or bi-weekly payments and provide the purchaser with the option of buying the car at the end of an agreed upon period. Repayment terms can also vary in the way in which the loan is amortized. Some contracts may require a full amortization of the loan; others may defer part of the payments into a balloon payment at the end of the loan term.

Default Conditions

Last but not least is the condition of default. A default condition is any stipulation that makes the entire agreement void. Most auto loan agreements include default conditions that encompass the following situations: A default condition must be stated in the agreement and the conditions clearly spelled out to the borrower.

How to Interpret an Auto Loan Agreement

Whether you are purchasing a new or used car, financing a vehicle purchase involves signing an auto loan agreement and related legal documents. This contract obligates you to pay the lender back with interest over a set period of time. If your payments fall behind, the lender could repossess the vehicle.

Reading the auto loan agreement and asking questions of the lender before you sign is a good way to ensure you are on track to make all your payments, avoid expensive fees and ultimately keep this potential debt in good standing.

Read the document carefully. – You will sign many documents when you buy a vehicle. Always read each one carefully so you know what obligations you are taking on.

Don’t be afraid to ask questions. – If you don’t understand something, ask someone to explain it to you.

Pay attention to late fees. – In the case of an auto loan agreement, late fees are common. You should make sure you know what these are so you can avoid them.

Be cautious with the down payment. – Make sure you have enough left after your down payment to afford the monthly payments.

Be wary of prepayment penalties. – Some auto loan agreements contain high penalties for prepaying the loan. Avoid these deals if possible.

Decoding Interest and Fees

Interest rates and fees are unwavering components of an auto loan agreement. To understand how interest rates are entered into the loan agreement, consider the three types of interest rates: simple, fixed-rate and variable-rate.

Simple interest

A simple interest rate is one of the most straightforward interest rates. With this type of interest rate, you know exactly how much you will pay for your car loan. When your car loan is paid off in full, you owe the total amount of your loan. Throughout the life of the loan, you only ever pay the interest on the remaining balance of your loan. Most banks use simple interest on car loans, so simple interest is most common.

Fixed-rate

A fixed-rate agreement means the bank agrees up front to charge a constant interest rate over the life of the loan. Your monthly payment will not vary according to the interest rate, and the interest rate can not change throughout the loan. Even if market interest rates fluctuate, you are only responsible for the fixed-rate on your loan. Fixed-rate auto loans are the most common type of auto loan.

Variable-rate

With a variable-rate auto loan, the bank reserves the right to 변경 your interest rate if current interest rates change. Your monthly payment may change as well as the amount of your total payments. When the bank raises your interest rate, they do so by changing the interest rate on your outstanding balance. The downside to variable-rate loans is that the increase may be small or large, making it difficult to predict your total cost of the loan. On the other hand, when interest rates fall, your lender may lower your rate.

Finding a great deal on the addition of interest rates and fees can save you money over the life of your loan.

Borrower’s Rights and Obligations

When you author an auto loan agreement, it should come with explicit rights and responsibilities for both the creditor and the debtor. For the borrower, their rights will start with the freedom of use of the vehicle. They should be able to enjoy that vehicle however they see fit almost every day of the week. In some states, there may be restrictions on the number of miles they can drive in a year to prevent them from depreciating the vehicle’s value at an unreasonable rate.

No matter how they use the vehicle, the borrower has the right to pay off the loan early. If they choose to do this, some creditors will charge an early payment penalty. In most cases, an early payment penalty is a percentage of the principal balance. You have some discretion in what that penalty rate should be.

The borrower’s most basic of requirements is to make timely payments on the loan. A creditor has a lot of legal recourse if the borrower misses just one single payment. But there are certain basic requirements for the borrower in every auto loan agreement . One of those is to preserve the value of the car. Generally, the borrower should keep the car insured against loss or damage.

If the car is damaged in an accident or vandalized, the borrower may need to file a claim with their insurance company and you cannot object to that. But if a borrower is intentionally negligent with a car, then you can repossess it as soon as it is not timely returned. Most car loan contracts will give you permission to repossess and reclaim the car at any time, even if the borrower is not late on payments.

A borrower should never alter the car. There may be community ordinances or building codes that limit the extent of modifications. Unauthorized modification of a car can result in repossession. You also have the right to repossess a car if the borrower gets behind on payments.

An auto loan contract may have several other rights and conditions that apply to both the creditor and the borrower. It’s a good practice to get sample agreements before selecting a contract to use. Getting a sample auto loan agreement online is really easy.

How to Craft a Custom Auto Loan Agreement

Creating a customized auto loan agreement is a crucial process to ensure the protection of both the lender and the borrower. The agreement should outline the key elements of the loan transaction while also complying with legal requirements. When drafting the agreement, start by including basic information about the parties and the vehicle, as well as the terms of the loan such as the amount being lent and the interest rate. It’s also important to highlight the identification of the borrower and the lender, including all needed addresses. Terminology should be used consistently and effectively to avoid any misunderstandings.

While using a pre-drafted template may save time, it’s essential to modify the language to fit the specific circumstances and parties involved. Creating a unique auto loan contract that fairly addresses the needs of the lender and the borrower can help function as a reference point in the event of a dispute, whether that dispute is over the loan terms themselves or the ability for either party to pay off or collect the loan. This document can serve as a powerful tool to ensure the loan is enforced on legal grounds.

Pitfalls in Auto Loan Agreements

While most auto loan agreements include the basic elements required for a valid contract, lenders frequently include clauses or features that can give rise to disputes. Some common mistakes include:

Failure to Identify Vehicle If a vehicle is not specifically identified in the loan, this can lead to issues regarding the vehicle and the property being financed. A good example of this is where the buyer intends to purchase a car from the seller, but the seller later changes his mind. In a contract of sale, the buyer has an irrevocable right to the property, while the seller has a limited right of repossession. However, if the agreement only specifies that the buyer will pay the total price after receipt of the vehicle, the contract may not be enforceable because the subject matter is not sufficiently identified. If the loan agreement does not identify the vehicle to be purchased, the lender may have a right of setoff or repossession. Generally, any loan contract that states "entrusts" the money to the borrower is not enforceable as a sale. Instead, it is considered as a loan in which the money is entrusted to the buyer to purchase the named property, and where the buyer retains the freedom to spend the money as he/she deems necessary. In this situation, the borrower can use the money to purchase non-related property, leaving the lender with no recourse.

Personal Guarantees Sometimes, auto sales occur between family members. In such cases, if the loan agreement is signed by a corporation, and the owners sign it as "personal guarantors," the agreement is not valid. In other words, the corporation is not bound by the contract. Often, employees who are involved in negotiating the sale of the property sign the agreement as "authorized agents" for the corporation. However, the corporation is not liable for the obligations of its agents, and even though the contract may be legal, the corporation is not bound.

Signing Under Special Capacity Many businesses provide people who are authorized to sign contracts on behalf of the company. Contracting with such an organization is similar to executing a contract with an individual, and requires the signature of the company’s owner, or of individuals authorized to contract on behalf of the corporation. If the individual signing the agreement does not have this authority, the loan agreement will not be enforceable on behalf of the company. In this situation, the corporation has two choices: 1) the corporation can approve of and ratify the contract, or 2) the corporation can avoid the contract. Orlando Auto Loan Agreements have a section that reduces the risk of the corporation avoiding the contract by requiring that the corporation waive all defenses that may arise.

No Right to Cure In many states, lenders must provide borrowers with the opportunity to cure their defaults as a condition of enforcing the loan terms, but the auto loan agreement often lacks a clause stating whether a right to cure exists or not. If this section is omitted from the auto loan agreement, the borrower can raise the "failure to cure" defense and the lender will be unable to recover. The Orlando Auto Loan agreement provides for the borrower’s right to cure prior to repossession.

No Default Notice Most lenders do not give notice of default in an automobile loan agreement. If there is no specific provision in the contract, the receiving party has no obligation to give notice. The Orlando Auto Loan agreement has a provision that states that the borrower waives the need for default notices, allowing the lender to seek prompt repossession.

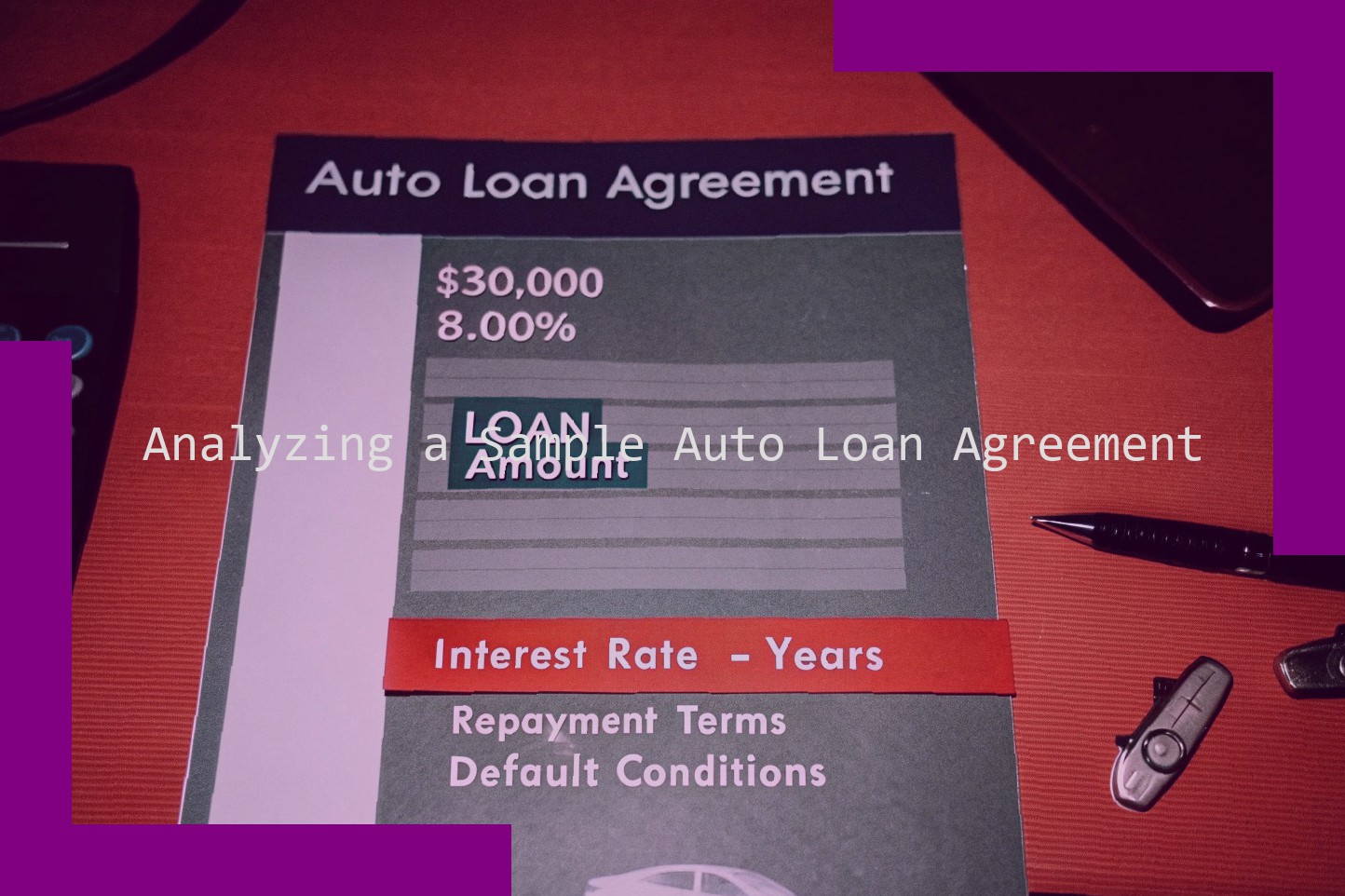

Example Auto Loan Agreement Template

Here’s a sample auto loan agreement template:

LOAN AMOUNT:$30,000.00

INTEREST RATE:8.00%

TERM: 5 years (60 months)

AMOUNT DUE PER MONTH:$606.44

This is not a legally binding document but is an example of a typical loan agreement. Your agreement may vary depending on your lender’s policies, but the general components remain the same.

Again, an auto loan agreement will typically contain this basic information:

The loan amount is the total amount of money you’re borrowing to purchase your vehicle. This does not include sales or excise taxes , which are included in the price of your vehicle.

The interest rate is the rate your lender charges you for borrowing money. It can be assessed daily, weekly, quarterly, monthly or annually.

The term is how long you have to repay the loan. It typically ranges from 3 to 7 years.

The amount due per month is how much you pay each month until the 5-year term expires. At that time, you must repay the entire remaining balance, including any interest accrued in the interim.